Structure

The VGSF program is a 5-year, full-time program that is structured into coursework and research. The aim of the coursework is to equip students with the tools necessary to develop innovative research in finance.

VGSF students are fully funded, allowing them to completely focus on their PhD.

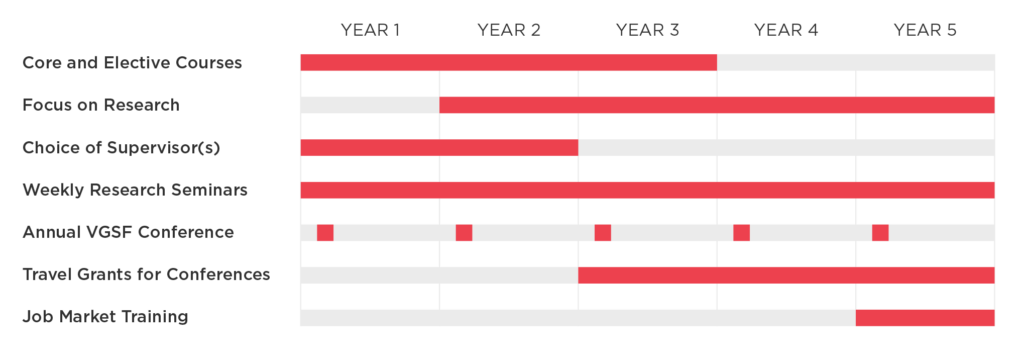

Core & elective courses

In the first three years of their PhD studies, students take a range of courses, which include core and elective courses. To find out more about courses, please click here.

Research

In their third year, students start focusing on research. Our students are required to write three research papers, including one single-authored paper.

Choice of research area(s) & supervisor(s)

Students generally choose their supervisor(s) in their second year, after developing their research interests. Our faculty’s research areas include corporate finance, asset pricing, financial intermediations, and market microstructure, among other fields. To find out more about our faculty, please click here.

Weekly research seminars

Every week, VGSF organizes the Finance Research Seminar, hosting top international researchers presenting their current work. This weekly event introduces our students to innovative research ideas and to a wide network of finance scholars.

Additionally, students and faculty can join the seminars organized by WU’s Department of Finance, Accounting and Statistics and the University of Vienna’s Faculty of Business, Economics and Statistics.

VGSF Conference

This annual conference provides students with the opportunity to present their research and progress to the entire VGSF faculty and receive valuable insights and feedback. The two-day conference includes a networking dinner.

Travel grants for conferences

Students whose papers are accepted for presentation at major conferences are eligible for travel grants. In addition, students can attend local seminars and events organized by the supporting institutions.

Job market training

In the fifth year, we help students prepare for the job market with job market training sessions, mock interviews, and a seminar on presentation skills.

VGSF Brochure